Venture Blues

- Author

- Keith Teare

- Published

- Fri 25 Apr 2025

- Episode Link

- https://www.thatwastheweek.com/p/venture-blues

Show Notes: Venture Blues: Cloud, Silver Lining

Overview

This week’s “Venture Blues” editorial brings into focus a brewing transformation in early-stage venture capital. As funds endure stretched timelines and mounting LP pressure, long-taboo secondary markets are stepping into the limelight. At the same time, traditional VC structures—anchored to power-law home runs and decade-long illiquidity—are under fresh scrutiny.

What makes this collection compelling is its blend of on-the-ground investor testimony (from Dan Gray, Hunter Walk, Rob Hodgkinson) and hard data (Carta charts, Series B MOIC trends) that together sketch a venture asset class at a crossroads: can it engineer better liquidity and more dependable returns without sacrificing outsized upside?

Key Trend 1: The Liquidity Imperative and Rise of Secondaries

As portfolio companies stall in late-stage rounds, early-stage VCs and LPs alike are waking up to the need for earlier liquidity—and rediscovering secondaries.

Why it matters:

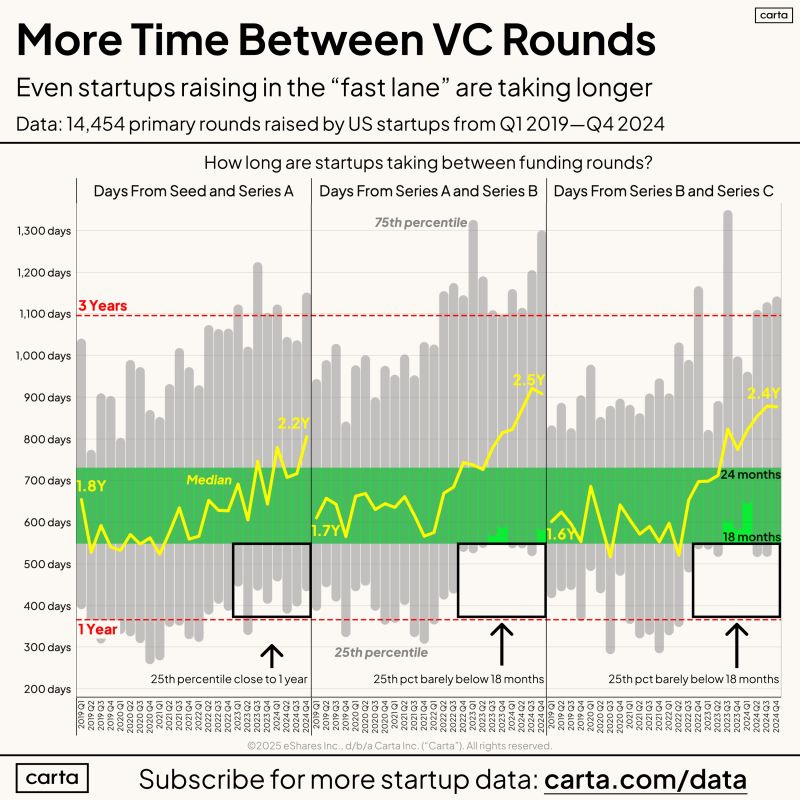

– Stigma around selling GP stakes is eroding when 10-year fund cycles stretch toward 15 years.

– Liquidity becomes critical to meet IRR targets and redeploy capital.

Talking Point 1: From Taboo to Toolbox

Quote:

“The obvious desperation for liquidity has — for now — removed the stigma associated with secondaries.”

— Dan Gray’s X post

Early-stage managers, once loath to let shares go, now view secondaries as a legitimate value-preservation tactic.

Removing psychological barriers makes secondaries a core liquidity channel, not just a last-resort option.

Talking Point 2: Fund Cycles Stretch, LP Calculations Shift

Quote:

“For the earliest funds (pre-seed, seed) this means instead of 10 year fund cycles for LPs, you’re seeing closer to 15, which fundamentally changes LP calculations about the asset class.”

— Hunter Walk, Homebrew

Longer holding periods erode IRRs and cash-on-cash returns.

LPs factor in delayed distributions, pressing GPs to surface secondary opportunities sooner.

Key Trend 2: Structural Challenges in Traditional VC Models

Despite aggregate Series B investments growing 476% over eight years, most value remains on paper—and out of reach.

Why it matters:

– Healthy MOIC doesn’t equate to real cash returns.

– Most LPs lack access to top-performing funds and can’t live off latent value.

Talking Point 1: MOIC vs. Cash—The Distribution Dilemma

Quote:

“And the 4.76x is measured in MOIC, not cash, so was not distributed.”

— Venture Blues editorial

Venture’s celebrated power law produces massive paper returns skewed toward a handful of winners.

Without distributions, LPs can’t recycle gains, creating a false sense of asset-class health.

Talking Point 2: Concentration of Compelling Managers

Quote:

“Most LPs do not get returns, and certainly not liquid returns (the only real kind).”

— Venture Blues editorial

A small club of star GPs capture most performance.

Broader LP community remains exposed to illiquidity without average outcome participation.

Key Trend 3: Rethinking the LP Base and Investor Alignment

Economic uncertainty is forcing a recalibration of who backs VC—and how.

Why it matters:

– Traditional LPs (endowments, pensions) face funding pressures.

– New entrants (sovereign wealth, retail, alternatives platforms) demand different structures.

Talking Point 1: Endowment Exodus to Secondaries

Quote:

“A harbinger of change is Yale, who pioneered the ‘endowment model’… selling $6 bn in its PE portfolio in secondaries for the first time.”

— Rob Hodgkinson

Endowments under the gun from taxes, tariff impacts and political hostility.

Liquid strategies gain priority, reshaping demand for evergreen and secondary vehicles.

Talking Point 2: LP Preferences Shape Fund Products

Quote:

“VC is changing. Venture firms need to rethink not just who they raise from, but how their LP base influences what they’re offering.”

— Rob Hodgkinson

A move toward evergreen, co-invest, direct, and secondary funds rather than classic 10-year vehicles.

Funds must tailor structures to new LP appetites for liquidity and risk profiles.

Key Trend 4: Emerging Structures for De-Risked, Liquid VC Investments

Algorithmic selection and private-company indexes promise to lower risk, broaden access and embed liquidity.

Why it matters:

– De-couples returns from a small set of GPs and rare unicorns.

– Creates tradable vehicles for average VC outcomes.

Talking Point 1: Filtering the 7% That Matter

Quote:

“Investing in this 7% as an index gives investors the ability to participate in de-risked average outcomes.”

— Venture Blues editorial

Data and machine learning reject 93% of Series B rounds.

The top 7% deliver 6.2x MOIC in five years, enabling an index tilted for performance.

Talking Point 2: Liquidity by Design

Quote:

“There is no longer a dependency on which fund an LP can invest in… And liquidity is built into the index approach.”

— Venture Blues editorial

Index shares can be bought and sold once listed on public markets.

Retail investors and non-traditional allocators gain direct VC exposure.

Discussion Questions

How has the elongation of fund cycles from 10 to 15 years altered LPs’ appetite for early-stage VC?

Can the rise of secondaries truly resolve liquidity challenges, or does it merely shift them to later rounds?

With secondaries becoming “primary” for early-stage VCs, is there a risk of misaligned incentives between GPs and founders?

How might new LP entrants (retail platforms, sovereign wealth funds) reshape venture fundraising and governance?

Is algorithmic selection and index-based investing a silver bullet for de-risking VC, or does it introduce new systemic biases?

Is the core issue in venture the lack of liquidity or the inherent power-law structure forcing “home runs”?

What unintended consequences could emerge from tradable private-company indexes?

Closing Segment

Venture Blues reveals an asset class in flux: the thirst for liquidity is rewriting norms, LPs are demanding new structures, and data-driven models offer a glimpse at more equitable, de-risked returns. As we watch secondaries soar and index products emerge, the central question remains: can VC evolve beyond its 70-year blueprint to deliver both outsized growth and true liquidity?

Final thought: the silver lining in today’s venture clouds may be a fundamentally redesigned asset class that finally brings average, liquid outcomes within reach.

Stay tuned as we track which of these trends will reshape the venture landscape for good.

This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.thatwastheweek.com/subscribe