🎙️ Audit by Neeraj

Audit by Neeraj Arora

- Update frequency

- every 24 days

- Average duration

- 14 minutes

- Episodes

- 45

- Years Active

- 2020 - 2025

CA Inter Audit Chapter-1 Class 1 & 2

In this podcast, we will revise Few topics of Chapter-1.

Basics Covered-

* Meaning and Nature of Auditing

* Audit Objective & Opinion

* Misstatement

* Materiality

* Applicable Financial Reporting Framework…

CA Inter Audit Chapter-3 Audit Risk & Risk Assessment Part-2

🚀 CA Inter Audit Podcast: Mastering Audit Risk & Risk Assessment! 🎧

In this episode, we dive deep into Chapter 3 – Audit Risk and Risk Assessment for CA Inter Audit exams. 📚

We will discuss SA 315 Iden…

CA Inter Audit Chapter-3 Audit Risk & Risk Assessment Part-1

🚀 CA Inter Audit Podcast: Mastering Audit Risk & Risk Assessment! 🎧

In this episode, we dive deep into Chapter 3 – Audit Risk and Risk Assessment for CA Inter Audit exams. 📚

Gain clarity on:

✅ Meaning …

CA Inter Audit Chapter-11 Ethics & Terms of Engagement Part-2

We’ve released a new podcast on Chapter 11 – Ethics & Terms of Engagement to help you revise on the go! 🎙️ This scoring chapter (10-11 marks in ICAI exams) is crucial, so make sure you go through it …

CA Inter Audit Chapter-11 Ethics & Terms of Engagement Part-1

🎙 Welcome to the CA Inter Audit Podcast – Ethics & Terms of Engagement!

In this episode, we discuss key topics from Chapter 11 – Ethics & Terms of Engagement, an important and scoring chapter in ICAI …

SA 580 Written Representation Podcast | Audit Podcast by Neeraj Arora

In this podcast, we will be discussing about SA 580 Written Representation.

A written representation is a written statement by management provided to the auditor to confirm certain matters or to suppo…

SA 265 Communicating Deficiencies in Internal Control to Those Charged with Governance & Management

In this podcast, we will be discussing SA 265 Communicating Deficiencies in Internal Control to Those Charged with Governance & Management.

SA 265 deals with the auditor’s responsibility to communicat…

SA 320 | What is Materiality in Auditing? | Materiality क्या है?

In this podcast, I have discussed the “Concept of Materiality”. Following topics have been discussed in the podcast-

SA 320 deals with the auditor's responsibility to apply the concept of materiality …

SA 300 Planning an Audit of Financial Statements | Audit Podcast | Audit by Neeraj

SA 300- Planning an audit of financial statements deals with the auditor's responsibility to plan an audit of financial statements. It states that objective of the auditor is to plan the audit so tha…

Basics of Audit Part-3 | CA Intermediate | Neeraj Arora #Auditislove

In this podcast, I have discussed the “Basics of Auditing”. Following topics have been discussed in the podcast-

* Basic understanding of Internal Control

* Meaning

* Examples

* Why are internal controls…

Basics of Audit Part-2 | CA Intermediate | Neeraj Arora #Auditislove

In this podcast, I have discussed the “Basics of Auditing”. Following topics have been discussed in the podcast-

* Type of Opinion - Clean and Modified Opinion

* Qualified, Adverse and Disclaimer of Op…

Basics of Audit Part-1 | CA Intermediate | Neeraj Arora #Auditislove

In this podcast, I have discussed the “Basics of Auditing”. Following topics have been discussed in the podcast-

* Meaning of Audit

* Objectives of Audit as per SA 200

* Meaning of Misstatement

* Meanin…

Is it compulsory to write in ICAI Study Material language?

In this podcast, you'll learn about the language style you should use when answering questions in the CA Exams held by ICAI.

With the May 2024 exams coming near, many students are wondering how they …

How to Study CA Inter Audit for ICAI May 2024 Exams?

In this podcast, we're going to talk about how to get ready for the CA Inter Audit exams happening in May 2024. Since the exams are getting closer, students are feeling nervous about how to prepare &…

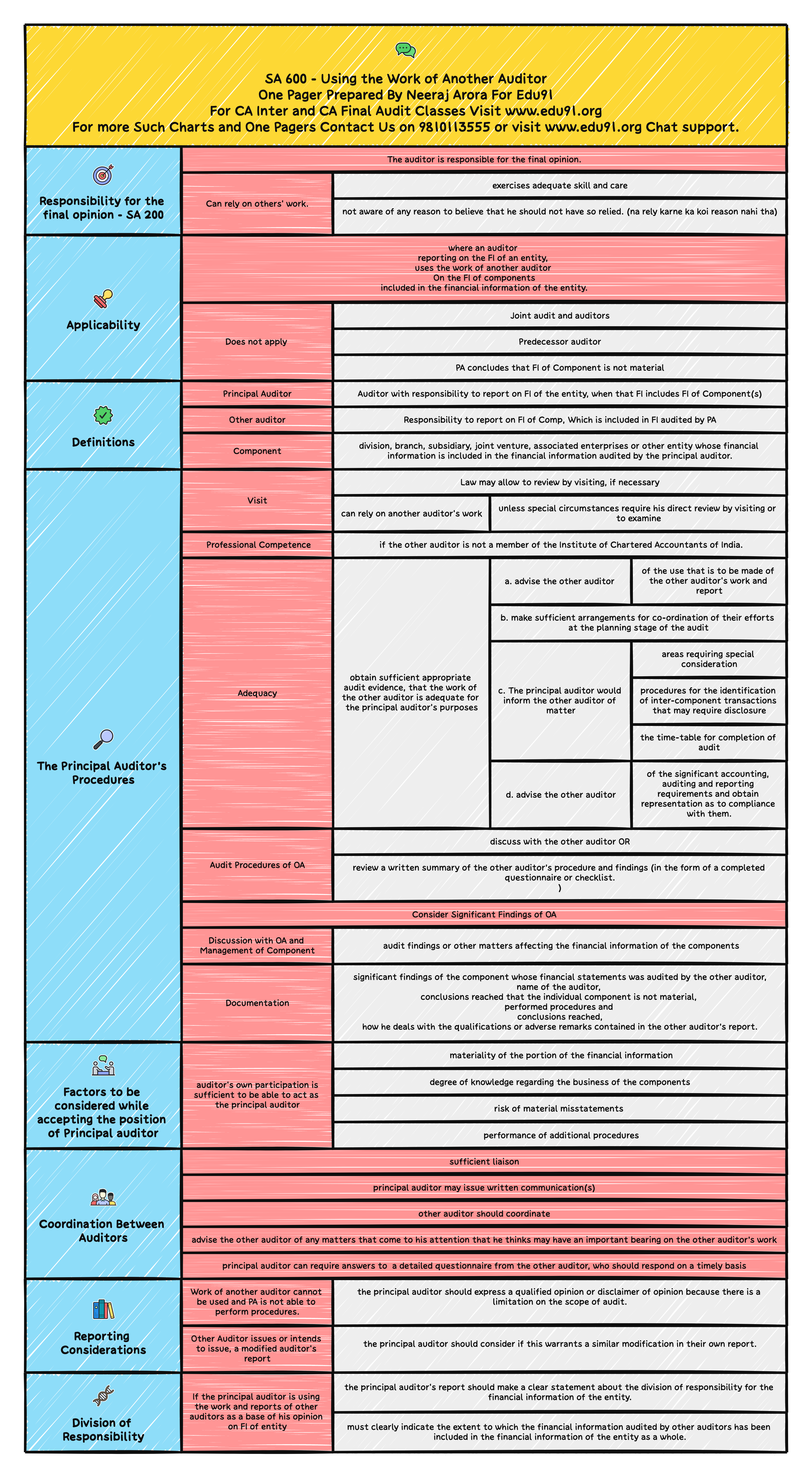

31 SA 600 Using the Work of Another Auditor

SA 600- Using the Work of Another Auditor

SA 200 Reference

Despite delegating work or using work of other auditors/experts, the auditor is responsible for the final opinion. Can rely on others' work, …

30 SA 560 Subsequent Events

SA-560 “Subsequent Events” deals with the auditor’s responsibilities relating to subsequent events in an audit of financial statements. Financial statements may be affected by certain events that occ…

29 Relevance of Audit Evidence With Example

Relevance means the relationship of the evidence with the audit procedure and the assertion being checked.

A given set of audit procedures may provide audit evidence that is relevant to certain assert…

28 SA 250

SA 250- Consideration of Laws and Regulation in an Audit of Financial Statements

Responsibility of Management for Compliance with Law and Regulations

It is the responsibility of management,

* with the o…

27 Risk assessment and Response With Example

Audit evidence to draw reasonable conclusions on which to base the auditor’s opinion is obtained by performing:

(a) Risk assessment procedures; and

(b) Further audit procedures, which comprise:

* Tes…

26. Test of Control

Test of control

Meaning

An audit procedure

* designed to evaluate the operating effectiveness of controls

* in preventing, or detecting and correcting, material misstatements at the assertion level.

Why…